12 Jun 2026

Most businesses treat payroll, accounting, and tax planning as three separate departments with three separate workflows. That's a costly mistake. In 2026, with the IRS tightening compliance requirements and multistate regulations growing more complex, running these functions in silos is one of the fastest ways to trigger penalties, fail audits, and leave real money on the table.

The businesses that stay protected, profitable, and fully compliant are the ones that integrate these three systems into one coordinated financial engine. This guide breaks down exactly how payroll accounting and tax planning work together and why that integration is the foundation of a sound business compliance strategy in the United States.

Why Integrated Financial Systems Matter in 2026

The U.S. regulatory landscape in 2026 has never been more demanding for employers. Federal payroll tax reporting requirements from the IRS, state-level wage and hour laws, and sales tax obligations for ecommerce businesses all converge on one fundamental truth: your numbers need to be consistent, accurate, and traceable from payroll to tax return.

When payroll, accounting, and tax planning operate in silos, errors compound. A payroll discrepancy becomes an accounting imbalance, which then becomes a tax filing problem. The IRS doesn't care which department made the mistake; the liability lands with your business.

Integrated accounting and payroll systems solve this by creating a single source of financial truth. Every payroll run automatically updates your books. Every accounting entry informs your tax position. Every tax strategy is grounded in real-time financial data.

The Cost of Siloed Financial Systems:

- Payroll errors lead to incorrect W-2s and 941 filings

- Accounting inaccuracies distort financial statements used for tax planning

- Missed deductions from poor coordination between bookkeeping and tax teams

- IRS audit risk rises when payroll data and tax returns don't reconcile

- Penalty exposure from misclassified workers or late deposits

The Three Pillars: How Each Function Works and Why They're Interdependent

To understand the integration, you first need to understand what each pillar does and what breaks when it's disconnected from the others.

Pillar 1: Payroll The Starting Point of Your Compliance Chain

Payroll is where your compliance obligations begin. Every pay period, your business calculates gross wages, withholds federal income tax, Social Security, and Medicare (FICA), and remits those taxes to the IRS on a strict schedule. State income tax withholding, unemployment insurance (SUTA), and local taxes layer on top of that.

The payroll tax reporting process doesn't end with the paycheck. Employers must file Form 941 quarterly, deposit withheld taxes on time, reconcile year-end W-2s and W-3s, and meet deadlines for FUTA (Form 940) annually. Miss any of these, and the IRS issues penalties that start at 2% for late deposits and can reach 15% for extended delinquency.

When payroll feeds directly into your accounting system, these numbers are automatically recorded as journal entries debiting wage expense and crediting tax liability accounts. That linkage is what keeps your books accurate and your tax filings reconcilable.

Pillar 2: Accounting The Accuracy Engine for Tax Filing

Accounting is what transforms raw financial transactions into meaningful, auditable records. Your bookkeeping and financial reporting function maintains the general ledger, categorizes income and expenses, tracks assets and liabilities, and produces the financial statements, including the income statement, balance sheet, and cash flow that your tax returns are built on.

Accounting data for tax filing is only as reliable as the bookkeeping behind it. Miscategorized expenses, unreconciled bank accounts, or uncaptured payroll liabilities distort your taxable income, sometimes inflating it (you pay more than you owe) and sometimes understating it (you're exposed to IRS penalties and back taxes).

When accounting is integrated with payroll, every pay run is automatically posted to the correct accounts. Benefits, garnishments, reimbursements, all of it flows into the ledger without manual re-entry. That means cleaner books, faster closes, and tax returns your CPA can prepare with confidence.

Pillar 3: Tax Planning Where Strategy Meets Compliance

Tax planning is not the same as tax filing. Filing is reactive; it reports what happened. Planning is proactive: it shapes what happens next to legally minimize your tax liability before the year ends.

Proactive tax planning strategies in 2026 include optimizing your business entity structure (S-Corp, LLC, C-Corp), maximizing retirement plan contributions, timing capital expenditures for Section 179 deductions, managing owner compensation to balance FICA exposure, and understanding how state tax nexus rules affect your multistate obligations.

Effective tax liability forecasting requires real-time financial data. If your accountant is working off books that are two months behind, the planning window closes before strategies can be executed. Integrated systems give tax planners the current-period visibility they need to act, not just report.

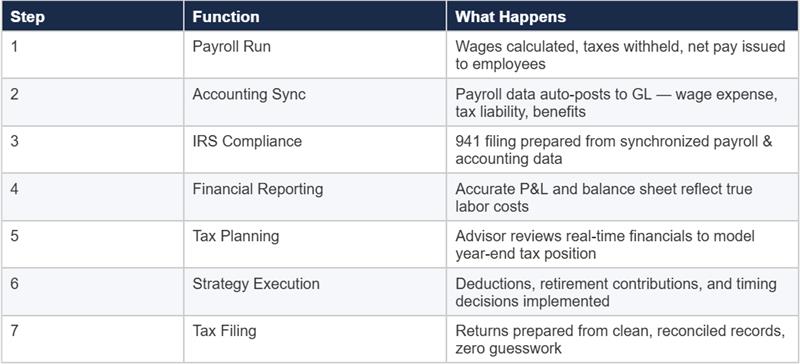

How Payroll, Accounting & Tax Planning Work Together: The Integration Flow

Here's how a properly integrated business financial compliance system operates in practice:

This integrated flow eliminates the manual handoffs, data rekeying, and reconciliation gaps that generate errors in siloed systems. More importantly, it reduces compliance risk at every stage, from payroll tax deposit deadlines to the accuracy of your annual business tax return.

IRS Compliance Requirements: What Your Business Must Get Right in 2026

The IRS has specific compliance requirements for employers that touch all three functions. Understanding these requirements clarifies why integration isn't optional; it's the only way to meet them consistently.

- Form 941 (Quarterly): Reports income tax withheld, Social Security, and Medicare taxes. Must reconcile exactly with your payroll records and general ledger.

- Form 940 (Annual): FUTA tax return. Calculated from total wages paid and state unemployment taxes credited, both of which live in your payroll and accounting systems.

- W-2 / W-3 Filing: Year-end employee wage statements must match 941 filings exactly. Discrepancies trigger IRS notices and can lead to penalties.

- 1099-NEC / 1099-MISC: Contractor payments tracked in your accounting system must be reported accurately. Misclassification (employee vs. contractor) is a top IRS audit trigger.

- Payroll Tax Deposits: The IRS deposit schedule (monthly or semi-weekly) is based on your lookback period liability. Late deposits incur penalties starting at 2%.

- Multistate Compliance: Businesses with employees in multiple states must manage state income tax withholding, SUI rates, and local taxes, each with its own filing calendar.

An IRS audit compliance checklist for 2026 should verify that payroll records, accounting entries, and tax return figures all reconcile to the same numbers. If they don't, you have an integration problem, and the IRS will find it.

Special Considerations: eCommerce, Startups & Small Businesses

eCommerce Businesses: Multistate Complexity Demands Integration

If you're running an ecommerce operation, whether on Shopify, Amazon, WooCommerce, or your own platform, your compliance footprint is significantly more complex than a traditional local business. Economic nexus rules, triggered by crossing sales thresholds in a state, create obligations for sales tax collection, payroll registration if you have remote employees, and state income tax filings.

Multistate compliance for ecommerce businesses requires your accounting system to track sales by state, your payroll system to manage withholding for employees across jurisdictions, and your tax planning strategy to account for apportionment rules that affect how your income is taxed at the state level. Without integration, this is nearly impossible to manage accurately.

Startups: Build the Right System Before You Need It

Startups frequently underinvest in financial infrastructure during early growth, then face a compliance crisis when headcount expands, or investor due diligence begins. A startup financial management system built on integrated payroll, accounting, and tax planning from day one saves you from the expensive cleanup that comes from building on a broken foundation.

The accounting system for startups should be designed with scalability in mind: cloud-based, connected to payroll, and structured to produce the financial statements that banks, investors, and the IRS will eventually scrutinize.

Small Businesses: The Most Exposed, the Most to Gain

Small business compliance in the USA is where integration pays its biggest dividends. Small businesses typically lack dedicated accounting or HR departments, which means the same person managing payroll is often the one doing the bookkeeping and trying to track tax deadlines. That's how mistakes happen.

Outsourced accounting and payroll services give small businesses access to professional-grade integrated systems without the overhead of an in-house team. The cost of outsourcing is almost always lower than the cost of a single IRS penalty, missed deduction, or compliance error.

Common Compliance Mistakes and How Integration Prevents Them

Understanding how to avoid compliance mistakes starts with knowing where they originate. Here are the most common failures we see in businesses running disconnected systems:

Compliance Failures and Their Root Causes

- Late payroll tax deposits: caused by manual tracking without automated reminders

- W-2 and 941 discrepancies: caused by payroll data not syncing to accounting

- Missed deductions: caused by bookkeeping that doesn't flag deductible expenses

- Worker misclassification: caused by no centralized system tracking contractor vs. employee status

- Incorrect state filings: caused by a multistate payroll not connected to state tax obligations

- Cash flow surprises at tax time: caused by no real-time tax liability forecasting

The solution to each of these problems is the same: real-time financial visibility across payroll, accounting, and tax planning. When all three systems share the same data, errors surface immediately before they become penalties.

What to Look for in an Integrated Business Compliance Partner

If you're evaluating accounting and payroll services in the USA, not all providers offer true integration. Here's what a full-service accounting firm with integrated capabilities should deliver:

- Payroll processing with direct sync to your general ledger, no manual data transfer

- Real-time bookkeeping and financial reporting with up-to-date account balances

- Proactive tax planning throughout the year, not just at filing time

- IRS compliance monitoring deadlines tracked, deposits scheduled, and filings prepared

- Multistate payroll and tax capabilities for businesses with distributed teams or an ecommerce nexus

- Worker classification review to reduce audit risk

- Business compliance consulting to identify and close gaps before they cost you

The best business compliance services in the USA function as a single, coordinated team, not a collection of vendors who don't talk to each other. TxProNext is built exactly that way.

The Bottom Line: Integration Is Your Compliance Strategy

In 2026, the question isn't whether your business needs payroll, accounting, and tax planning. Every business needs all three. The question is whether they're working together or working against you.

Businesses that integrate these functions gain real-time financial visibility, reduce compliance risk, avoid costly IRS penalties, and make better decisions because their numbers are accurate and current. Businesses that don't eventually pay the price in penalties, in missed opportunities, or in the chaos of an IRS audit they weren't prepared for.

The integrated business compliance system isn't a luxury reserved for large corporations. It's the standard every business should be operating with the right partner; it's more accessible than most business owners realize.

| Ready to Integrate Your Payroll, Accounting & Tax Strategy? Schedule a free consultation with TaxProNext today. We'll review your current systems, identify compliance gaps, and show you exactly what a fully integrated financial operation looks like for your business. Visit: www.TaxProNext.com |